Bad Housing Policy

Why Australian home prices are unaffordable

The financialization of housing in Australia has greatly inflated house prices beyond a reasonable amount and the government is still doing demand-side interventions despite it clearly being a supply-side problem.

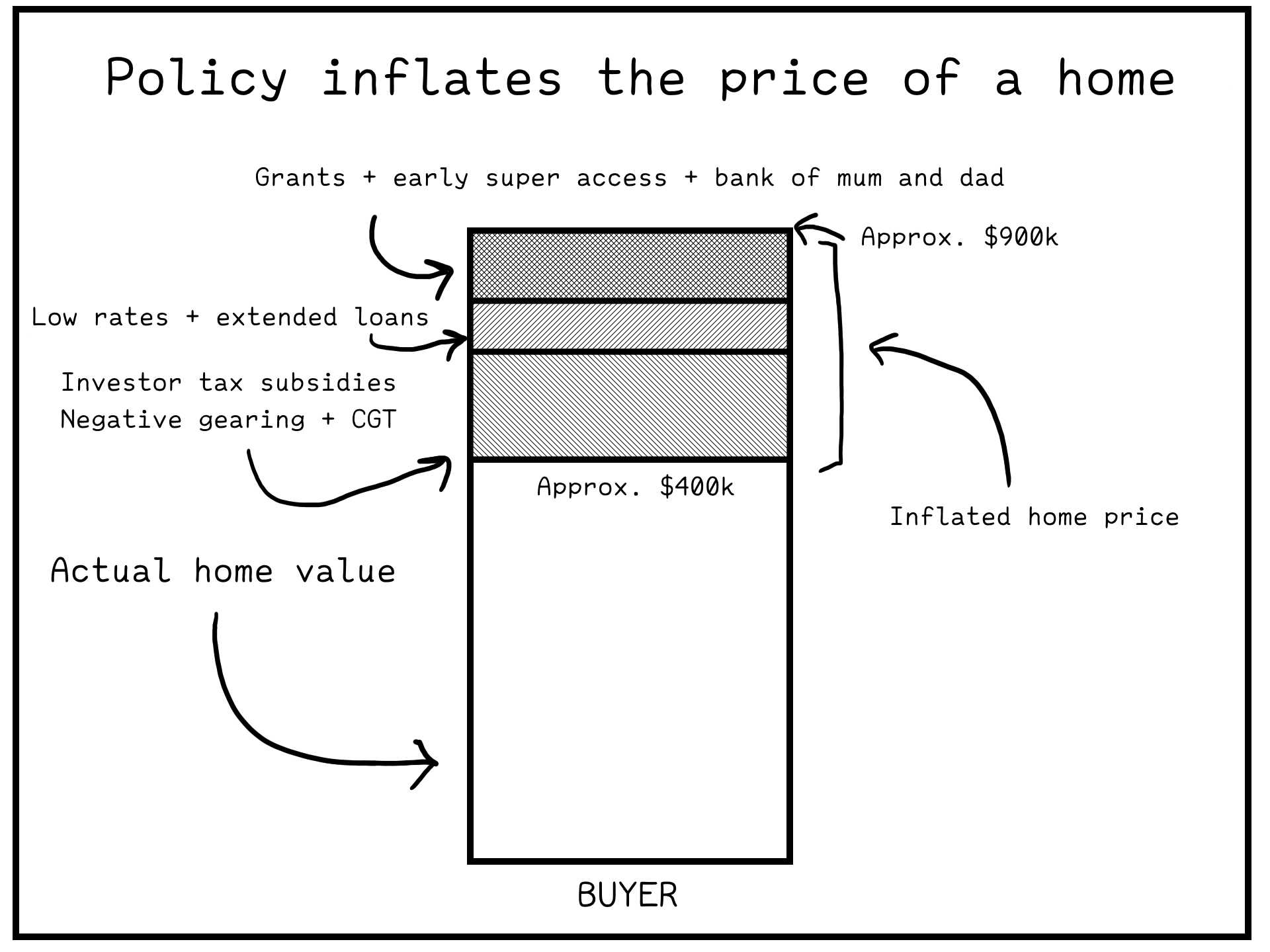

Policies like the "First home super saver scheme" or the "Australian Government 5% Deposit Scheme" are not addressing the underlying issue that home owners have been treating their homes as an investment vehicle. With home owners expecting a guaranteed return on their investment. This is despite the fact that with homes, just like any other investment, it is still possible to lose money. But since home owners don't want to incur losses on their investment and actually get a realized loss by selling their house below the purchase price, they have convinced the government to subsidize their investment by giving demand-side interventions.

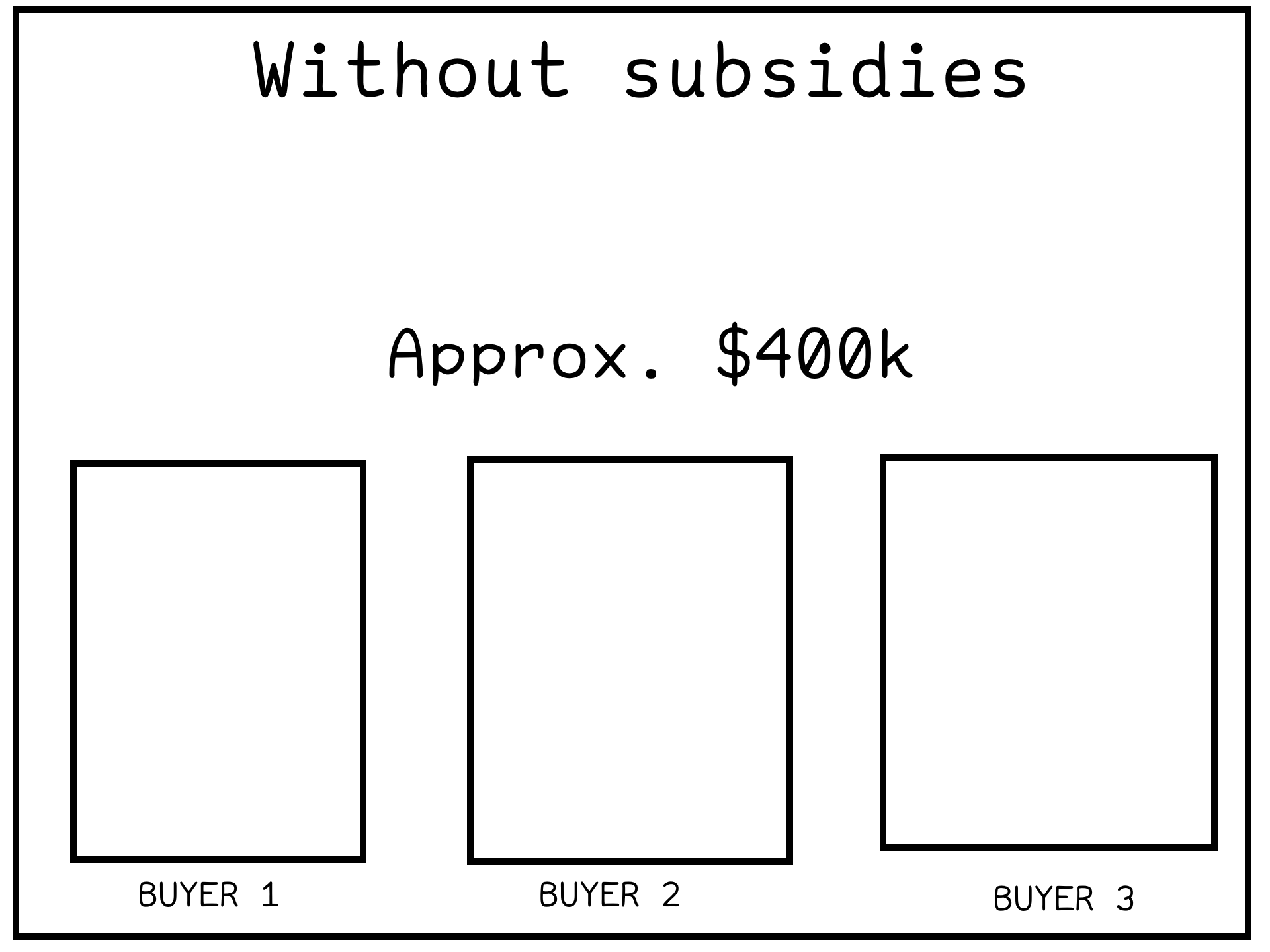

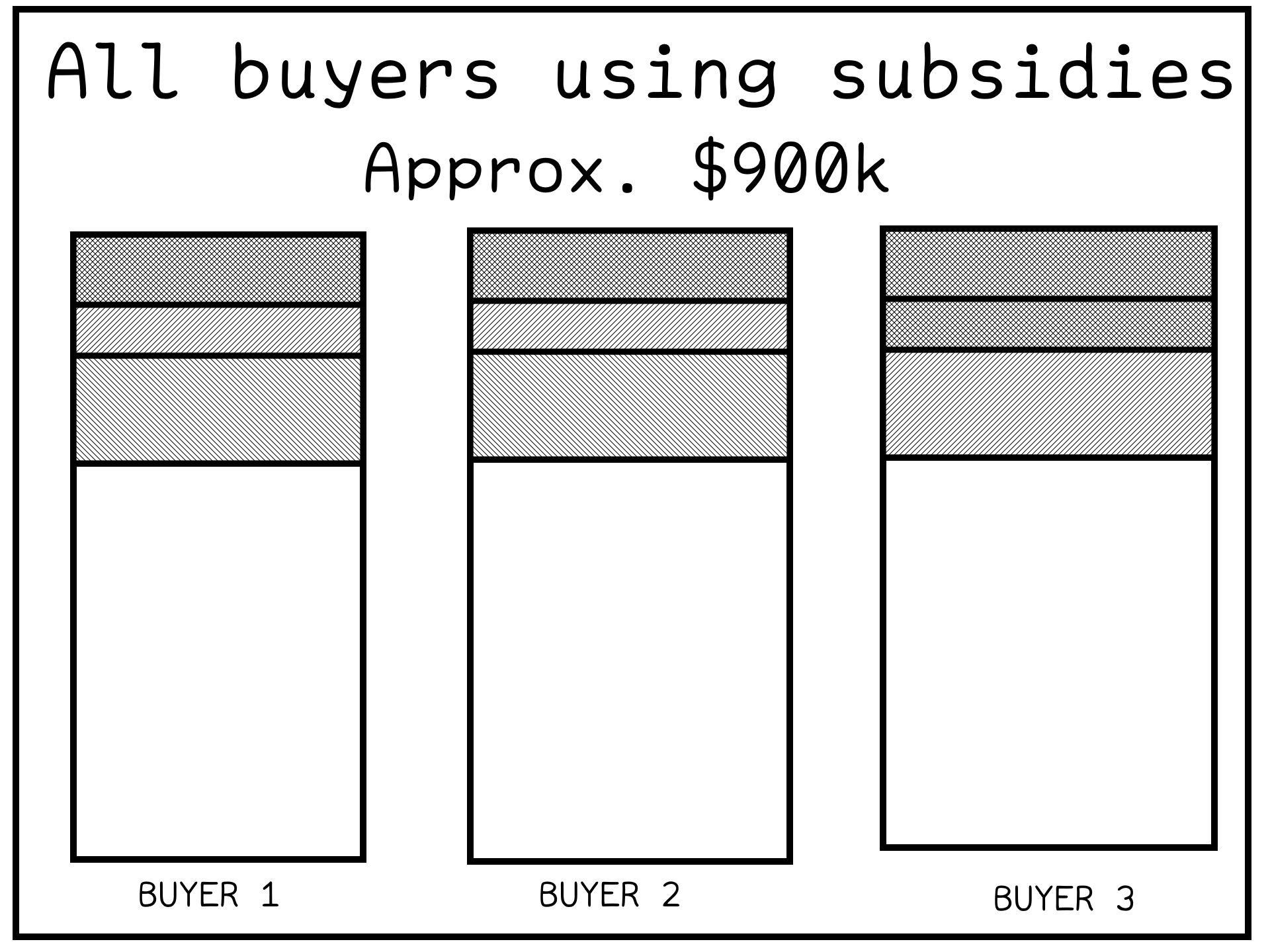

Adding more money on the demand-side has artificially inflated the home prices well beyond the actual value of the home. In addition to artificially raising the amount needed to purchase homes overall if you try to purchase without these subsidies. The expectation that home prices always rise has led to more overvalued home prices. Australian housing epitomizes greater fool theory, where people are buying overpriced homes to sell at an even greater profit at an ever increasing rate. The government keeps inventing new subsidies to fabricate and supplement these inflated home prices.

Instead of a 20% deposit, it is now a 10% deposit. No wait, it is now a 5% deposit. Instead of a 20-year home loan, it is now a 30-year loan. No wait, it is now a 40-year loan. Anything but for home owners to actually accept that they invested in an overpriced home and that they will need to accept a loss on that investment.

People may push back by saying that winding back negative gearing and the capital gains tax (CGT) discount will increase rents. But again, the market prices the rent. If no one can afford the rent set by the landlord, then the landlord must lower prices. Rent is not set by the landlord's CGT discount. Eventually landlords will price people out. Renters will end up moving back home with their parents and/or their grandparents as it becomes the only viable option. You cannot just keep squeezing renters, at some point they will realize that the percentage of their take-home pay going towards rent is unsustainable and will leave the rental market. Landlords are not entitled to renters.

Rent freezes and guarantee lease renewals will not solve this. Artificially lowering the price in a supply constrained market will not fix the root cause of this. If landlords cannot raise rent to the market rate they will either; exit the rental market by selling the property, reduce maintenance and improvement investments, only give out tenancies to lower risk higher income tenants, or find other ways to exit. This will reduce the supply of rental stock.

We need to remove the CGT discount and negative gearing. We need to abolish all demand-side subsidies. First home owner grants, super access for deposits, low deposit guarantee schemes all need to be rolled back. Each of these increases buyer purchasing power without increasing housing supply, preventing a market correction.